Late yesterday China released its April economic data and here’s the tale it tells of the property sector is of concern. New starts contracted 15% year on year (vs. -21.9% in March), property sales fell 14.3% year on year (vs. -7.5% in March); and land sales (by area) fell 20.5% year on year (vs. -16.9% in March). This chart is from Society Generale:

The greater risk to China lies in the pervasive consequences of any property bust. Property investment has grown to account for about 13 per cent of gross domestic product, roughly double the US share at the height of the bubble in 2007. Add related sectors, such as steel, cement and other construction materials, and the figure is closer to 16 per cent. The broadly defined property sector accounts for about a third of fixed-asset investment, which Beijing is supposed to be subordinating to the target of economic rebalancing in favour of household consumption.

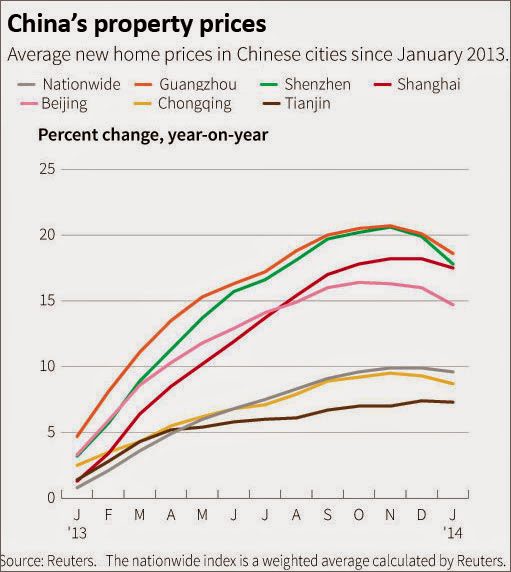

…The reason things look different today is the realisation of chronic oversupply. As the property slowdown has kicked in, housing starts, completions and sales have turned markedly lower, especially outside the principal cities. Inventories of unsold homes in Beijing are reported to have risen from seven to 12 months’ supply in the year to April. But when it comes to homes under construction and total sales, the bulk is in “tier two” cities, where the overhang of unsold homes has risen to about 15 months; and in tier three and four cities, where it is about 24 months.

…If activity levels and prices weaken further, Beijing’s resolve not to respond with traditional stimulus programmes is unlikely to hold. We should expect a potpourri that might include: extra spending on infrastructure and environment programmes; faster urbanisation in inland and western provinces; some relaxation on restraints on homebuying, such as mortgage deposits; and, ultimately, new monetary easing.